Contents

ToggleBlog 32-TReDS vs. GST Sahay: A Strategic Comparison for MSME Working Capital

TReDS and GST Sahay are both MSME financing mechanisms designed to improve business liquidity, but they work very differently and solve different financing needs. While TReDS focuses mainly on invoice discounting against approved invoices by the corporate, GST Sahay is more aligned toward GST and transaction-based working capital financing. This blog explains the practical difference between TReDS and GST Sahay, their business suitability, and common MSME use cases.

What is TReDS?

TReDS, or Trade Receivables Discounting System, is an RBI-regulated framework created to help MSMEs receive faster payment against invoices raised to corporates and PSUs. Under this system, MSMEs upload invoices on a TReDS platform after supplying goods or services. Once the buyer approves the invoice digitally, banks and NBFCs finance the invoice and MSMEs receive early payment before the actual due date.

The biggest advantage of TReDS is that financing mainly depends on the buyer’s credit profile rather than only on the MSME’s balance sheet. This helps MSMEs improve liquidity without depending entirely on traditional collateral-heavy working capital loans.

India currently has multiple RBI-approved TReDS platforms including RXIL, M1xchange, and Invoicemart.

MSMEs looking to understand:

- TReDS platforms,

- onboarding process,

- participants,

- and latest developments,

(Can read MSME TALK®’s detailed TReDS guide here:

https://msmetalk.com/blog/treds-platforms-in-india-structure-participants-and-latest-developments/)

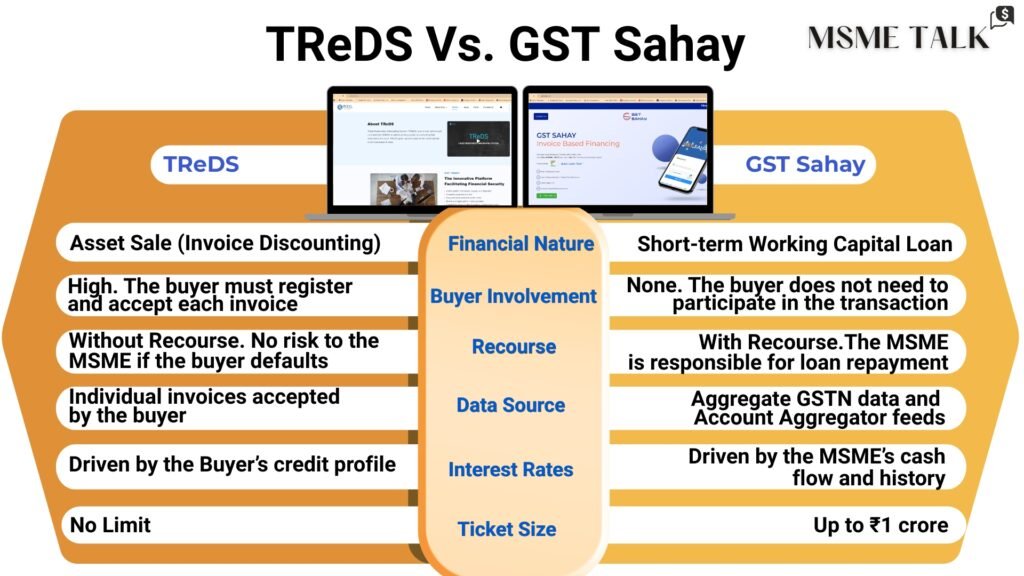

This mechanism is ‘Without Recourse’ to the MSME, meaning the seller is not liable if the buyer defaults after the invoice is discounted.

Readers can also explore MSME TALK®’s detailed article on RXIL, India’s first TReDS platform:

https://msmetalk.com/blog/blog-31-rxil-indias-first-treds-platform-for-msme-invoice-financing/

MSMEs preferring video format can also watch MSME TALK®’s discussion with CFOs of MSMEs in relation to TReDS and MSME invoice financing here:

https://youtu.be/s3feww6TGSY?si=7Wg-VFnuJ7iS41FU

What is GST Sahay?

SIDBI Sahay, also referred to in broader discussions as GST Sahay, is part of a digital MSME financing ecosystem associated with SIDBI.

Unlike TReDS, GST Sahay is not mainly dependent on approved corporate invoices. Instead, it focuses more on enabling smaller-ticket working capital financing using:

- GST transaction data,

- business transaction history,

- digital records,

- and cash-flow visibility.

The objective is to improve access to formal financing for MSMEs that may not necessarily supply to large corporates but still maintain active business operations and GST compliance.

GST Sahay leverages the Open Credit Enablement Network (OCEN) and the Account Aggregator framework to fetch real-time, consent-based financial data for instant loan processing.

TReDS vs GST Sahay: Main Differences

Which MSMEs Usually Use TReDS?

TReDS is generally more suitable for MSMEs that:

- supply to corporates,

- work with PSUs,

- operate in structured B2B ecosystems,

- and face long payment cycles.

Businesses commonly exploring TReDS include:

- manufacturing vendors,

- industrial suppliers,

- logistics providers,

- engineering companies,

- and enterprise service providers.

For such businesses, receivables often remain blocked for 30 to 90 days or more despite successful delivery of goods or services. TReDS helps improve cash-flow by enabling early realization of approved invoices. Above all these MSMEs can get invoice discounting at very good rate of interest as underwriting is based on the Buyer’s credit rating which are PSU or Corporate with higher credit rating than MSME Seller.

(Businesses evaluating invoice financing structures can also explore MSME TALK®’s detailed article on TReDS ecosystem here:

https://msmetalk.com/blog/treds-platforms-in-india-structure-participants-and-latest-developments/)

Which MSMEs May Prefer SIDBI Sahay?

SIDBI Sahay may be more suitable for businesses that:

- do not have large corporate buyers,

- require smaller operational funding,

- maintain GST compliance,

- and need faster working capital access.

This may include:

- traders,

- distributors,

- retailers,

- local manufacturers,

- and service businesses.

Such businesses may not always have large approved invoices suitable for TReDS, but they may still require short-term funding for:

- inventory,

- operational expenses,

- vendor payments,

- or cash-flow management.

Benefits and Limitations MSMEs Should Know

Both TReDS and SIDBI Sahay are useful MSME financing structures, but their usefulness depends on the business model, customer profile, payment cycle, and funding requirement.

TReDS: Benefits

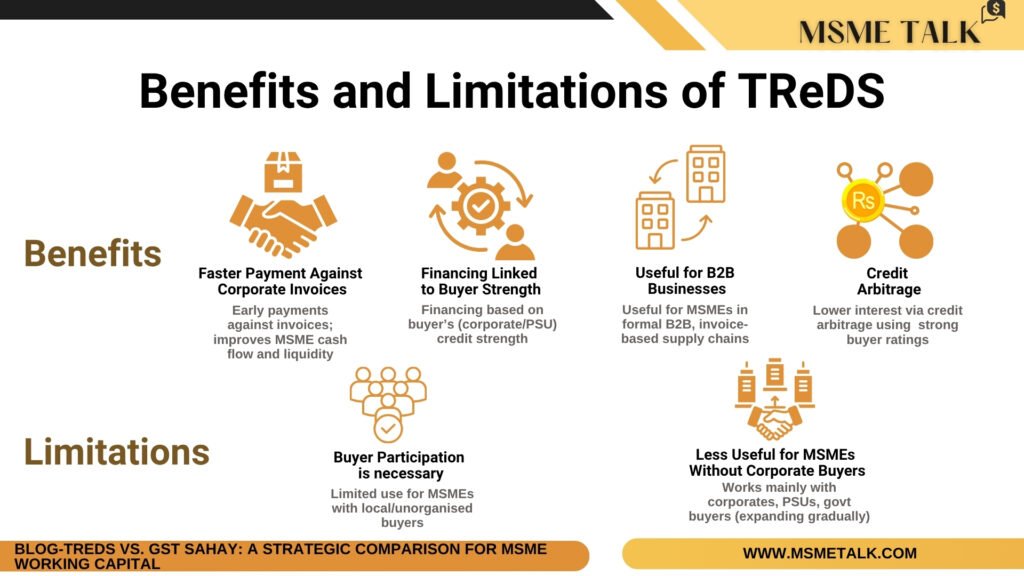

Faster Payment Against Corporate Invoices

TReDS helps MSMEs receive funds earlier instead of waiting for long payment cycles from corporates or PSUs. This improves working capital management and operational liquidity.

Financing Linked to Buyer Strength

Financing in TReDS depends more on the buyer’s credibility. MSMEs supplying to financially strong corporates may get access to comparatively better financing opportunities.

Useful for B2B Businesses

Businesses operating in formal supply chains with invoice-based transactions may find TReDS highly relevant for managing receivables.

Credit Arbitrage

Since credit is done on Buyer which are PSU or Corporate with higher credit rating than MSME Seller , MSMEs can get invoice discounting at a very good rate of interest which they will not get at their own credit.

TReDS: Limitations

Buyer Participation is Necessary

TReDS works effectively only when buyers actively participate and approve invoices on time. Without buyer approval, invoice financing cannot move forward.

Less Useful for MSMEs Without Corporate Buyers

Businesses supplying mainly to local markets or smaller buyers may not benefit significantly because TReDS is designed around B2B receivable financing. Currently restricted to transactions with registered Corporates, PSUs, and Government Departments. However, the ecosystem is evolving to include a broader range of buyers.

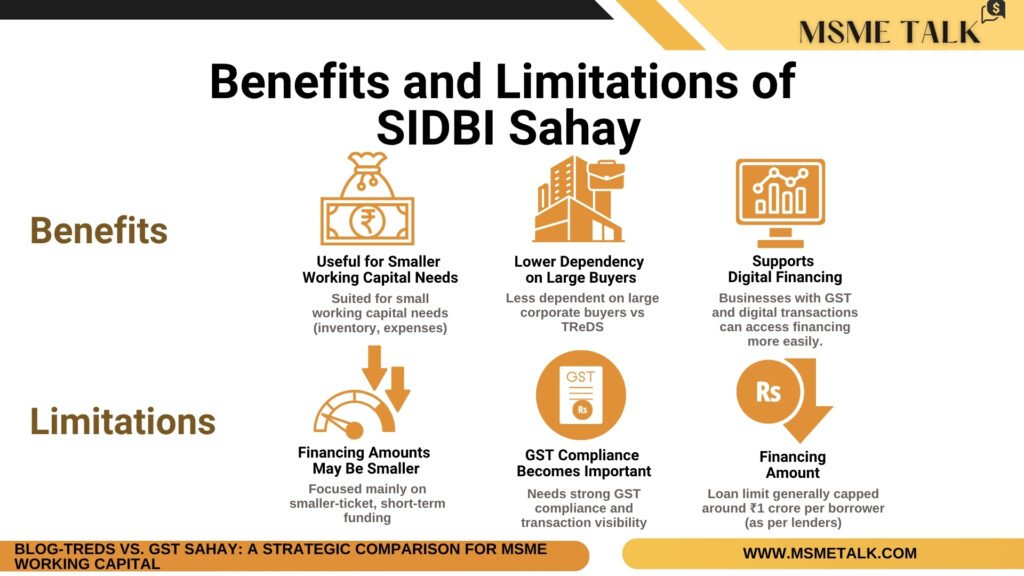

SIDBI Sahay: Benefits

Useful for Smaller Working Capital Needs

SIDBI Sahay is more suitable for MSMEs needing operational liquidity for inventory, business expenses, and short-term funding requirements.

Lower Dependency on Large Buyers

Unlike TReDS, financing is not entirely dependent on corporate invoice approvals. This makes it more relevant for smaller businesses operating outside large B2B ecosystems.

Supports Digital Financing

Businesses maintaining GST records and digital transactions may find transaction-based financing structures more accessible.

SIDBI Sahay: Limitations

Financing Amounts May Be Smaller

SIDBI Sahay is generally more aligned toward smaller-ticket operational funding rather than large receivable financing.

GST Compliance Becomes Important

Businesses with weak GST compliance or limited transaction visibility may face limitations in accessing transaction-based financing.

Financing Amount

GST Sahay’s ticket size limit is Rs 1 crore per borrower along with other criteria as per lenders.

Common Business Situations and Use Cases

Situation 1: Manufacturing Vendor Supplying to PSU

An MSME supplies products to a PSU with 60-day payment terms. The invoice is approved, but payment takes time.

In such situations, TReDS may help the MSME receive faster payment against approved invoices. In case of registered buyers, disbursal typically occurs within 24–48 hours of invoice acceptance.

Situation 2: Distributor Requires Inventory Funding

A distributor needs short-term funding before festive season demand. The business has GST records and regular sales activity but no large corporate receivables.

In such cases, SIDBI Sahay may become more relevant.

Situation 3: MSME Facing Delayed Corporate Payments

A supplier regularly faces delayed payments despite active business orders from Corporates.

TReDS may help improve cash-flow cycles by converting receivables into early liquidity.

(Businesses evaluating invoice financing can also read MSME TALK®’s detailed article on RXIL and TReDS ecosystem here:

https://msmetalk.com/blog/blog-31-rxil-indias-first-treds-platform-for-msme-invoice-financing/)

Situation 4: Small Service Business Needs Operational Liquidity

A service-oriented MSME requires smaller operational funding for salaries and ongoing expenses. The business may not have large invoice-based receivables but maintains GST records and digital transactions.

Transaction-based financing structures may become more suitable in such cases.

Situation 5: MSME Working with Multiple Small Buyers

A small manufacturing business supplies products to multiple regional distributors and retailers instead of one large corporate buyer.

In this case:

TReDS may become less practical because there may not be large approved receivables,

For fragmented buyer networks, GST Sahay provides superior operational flexibility compared to TReDS.

Things MSMEs Should Check Before Applying

Before choosing between TReDS and SIDBI Sahay, MSMEs should evaluate:

- whether buyers participate in TReDS,

- invoice approval timelines,

- Own GST compliance quality,

- financing requirement size,

- operational funding needs,

- repayment capability,

- and financing costs.

Businesses should also understand whether their financing challenge is mainly:

- delayed receivables,

or - lack of operational working capital.

This distinction is important while selecting the appropriate financing structure and cost of financing.

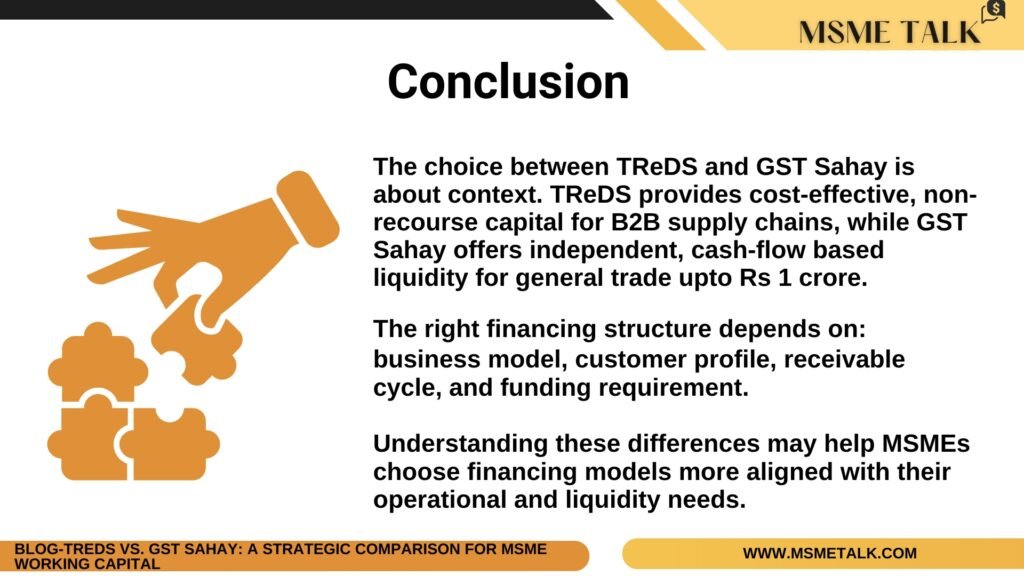

Conclusion

The choice between TReDS and GST Sahay is about context. TReDS provides cost-effective, non-recourse capital for B2B supply chains, while GST Sahay offers independent, cash-flow based liquidity for general trade upto Rs 1 crore.

Ensure your Udyam Registration is updated and your GST filings are accurate, as your data is now your most valuable collateral.

The right financing structure depends on:

- business model,

- customer profile,

- receivable cycle,

- and funding requirement.

Understanding these differences may help MSMEs choose financing models more aligned with their operational and liquidity needs.

For more insights like these and to stay updated on trends impacting MSMEs, Businesses and entrepreneurs follow MSME TALK on :

Stay Connected with MSME TALK®

- Watch & Learn: YouTube Channel

- Updates: Follow on LinkedIn

- Key highlights: Subscribe to Newsletter

Direct Access & Updates

- Broadcasts: Join our WhatsApp Channel (For latest news and trends)

- Alerts: Join our WhatsApp Group (For immediate updates and notifications)

- Queries: Message us on WhatsApp (For direct support)

Email Us

- connect@msmetalk.com